The turbulent UK cryptocurrency landscape sees the following report from the Financial Conduct Authority: 87% of crypto registration requests fail in the past budget year.

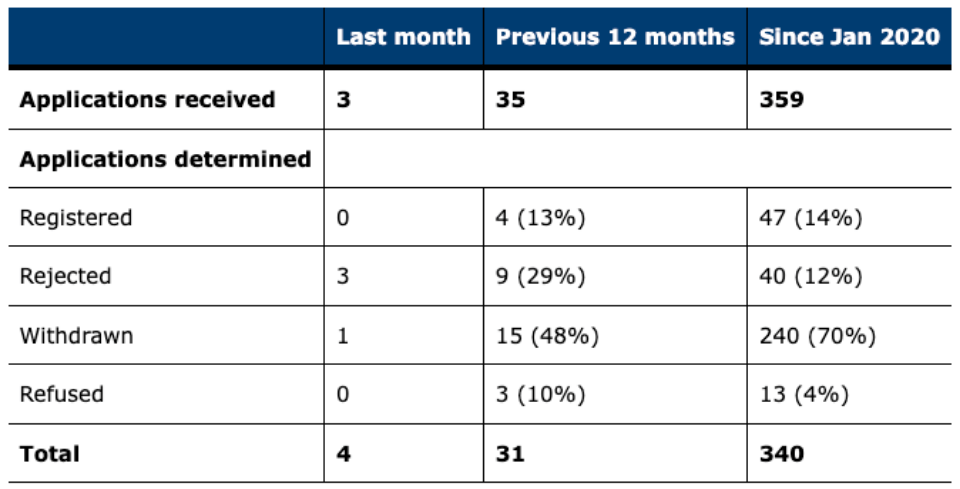

This is a shocking fact that raises very serious questions about the effectiveness of anti-money laundering measures in the sector. Only four out of 35 applications were approved, underlining how strict the regulations still are.

Struggling to meet standards

Since January 2020, the FCA has acted as a regulator for crypto companies, overseeing compliance with anti-money laundering, terrorist financing and money transmission regulations.

Overall, the report found that this high number of firms failed to meet the required standard. This was because most applications were rejected due to unsatisfactory fraud and AML checks, which are necessary to ensure that illicit funds do not enter the financial system.

The UK FCA denied the applications of nearly 90% of crypto registrations. Source: FCA

FCA Chairman Charles Randell noted:

“While some companies have demonstrated that their systems are adequate, too many have failed to meet acceptable standards of risk management and controls to date, leading to this wave of rejections and withdrawals.”

But the new regulations of the European Union, including Markets in Crypto Assets, or MiCA Frameworkhave made matters even more complex. Although these rules are aimed at better regulation of crypto assetsThey also add further complexity to UK businesses already struggling with local compliance issues.

With the regulations yet to be implemented, many are questioning whether the UK is still a viable market for crypto activities.

Why the FCA has rejected almost 90% of crypto firm applications https://t.co/4BgWSipEXw

— DL News (@DLNewsInfo) September 5, 2024

A new era of regulation

The FCA Report contributes to the larger initiative aimed at increasing regulatory oversight of the crypto sector. This includes the construction of a new “Crypto Cell” at the National Crime Agency with greater authority to deal with crimes related to cryptocurrencies.

This department is responsible for investigations and law enforcement support, underlining the government’s commitment to eradicating financial crime in this rapidly changing sector.

However, the FCA is so strict in its stance that crypto businesses are becoming frustrated. Many have complained of months of delays and insufficient feedback within the registration process.

Some companies have decided to move abroad in search of easier legal environments for their operationsyet still serving British customers. This issue raises questions about the UK’s competitiveness in the crypto space, at least for companies seeking friendlier regimes for their operations.

The Future of Crypto in the UK

Under the new Labour government, the future of crypto legislation is in limbo as the UK government shelve plans related to cryptocurrencies.

While the FCA plans to assist firms with the registration process, the high failure rate is an indication that there is still a long way to go before confidence and clarity in the system is built.

Pressure on governments and businesses to strike a balance between regulatory compliance and creativity is mounting as only 44 firms have actually registered since the FCA began overseeing the sector.

While the new rules under MiCA may provide a path to better governance, the UK crypto market is likely to remain troubled until then.

Main image from Pexels, chart from TradingView